Amazon Provision for Receivables Explained

Sarah Johnson

What Is Amazon Provision for Receivables, and Why It Keeps Distorting Your Vendor Payouts

If you have ever opened a Vendor Central remittance and found a payout lighter than expected, the problem is often not a classic chargeback. In many cases, Amazon has recorded a provision for receivables, which is typically a temporary accounting reserve that reduces the current payment while Amazon evaluates or awaits settlement of expected receivables, credits, or other account-level exposures. Understanding what is amazon provision for receivables matters because these reserves can tighten cash flow, complicate forecasting, and get misclassified as deductions that should be disputed immediately, even when the correct next step is to reconcile first and dispute second.

The line item vendors misread most often

At a practical level, a provision for receivables is commonly a reserve or holdback against amounts Amazon believes may become collectible from your account, or against amounts not fully settled yet. It is not always a final fee, and it is not automatically an error.

That distinction is the starting point for amazon vendor central payment deductions explained in a way that is actually useful. In Vendor Central, not every reduction in payout means the same thing:

A chargeback is typically a specific assessed deduction tied to a stated issue, such as routing, labeling, shortage, ASN-related noncompliance, or related operational items, depending on your program and terms.

A provision for receivables is usually a reserve based on expected liabilities, unsettled transactions, or perceived financial exposure that may later be reversed, applied, or adjusted.

A co-op or allowance deduction is often tied to agreed trade terms, marketing support, accruals, or promotional funding.

The difference between chargebacks and provision for receivables is important because the next action changes depending on what you are looking at. Chargebacks are generally issue-specific and evidence-based. Provisions are broader and often require you to ask what underlying exposure Amazon is trying to cover.

You can also see overlap in the underlying drivers. Returns exposure, shortage-related claims, co-op accruals, promotional costs, post-audit adjustments, and unresolved financial exceptions can all correlate with provision activity, although the exact mechanics can vary by vendor relationship and posting timing.

For experienced vendors, the real scope is bigger than one remittance line. Provision activity sits inside the broader amazon vendor central financial reconciliation process, which means you should tie it back to returns, shortage activity, trade agreements, freight compliance, disputes in progress, and timing gaps between accrual and settlement.

Why Amazon withholds money before the final bill is clear

The simplest way to think about a provision is this. Amazon may avoid paying out funds that it expects could be needed to cover future debits, offsets, or unresolved items.

That is a common answer to why is amazon withholding my payment for receivables. Amazon can reserve funds when it expects future debits, unresolved claims, or financial exposure that has not fully posted yet.

Expectation vs reality:

Expectation: “If Amazon deducted it, they must know exactly what it is.”

Reality: In many cases, Amazon can post a reserve before every underlying item is fully finalized in the remittance trail you can see.

This tends to show up in several situations.

Returns and post-sale exposure

If your catalog has elevated return activity, especially after seasonal spikes or a product issue, Amazon may reserve funds ahead of final returns processing or final offsets. This is one reason vendors in categories with high return volatility often see noisier remittances.

Shortages and operational claims

This is where an amazon 1p shortage claims and provisions guide becomes useful. Shortage claims themselves may appear as separate deductions or receivables activity, but if there is a pattern of unresolved shortages, receiving discrepancies, or proof-of-delivery mismatches, a reserve may appear while those items are sorted out.

Co-op, allowances, and promotional accruals

A lot of confusion comes from understanding vendor central co-op and provision fees together rather than treating them as interchangeable. Co-op is usually based on trade terms or marketing agreements. A provision for receivables may reflect Amazon’s expectation that some receivable, offset, or accrual-related activity will be collected or netted later. Vendors sometimes call this a “mystery fee” when it is often a timing and visibility problem.

Financial exposure tied to account activity

Sudden sales declines, account transitions, assortment changes, or unusual credit exposure can make reserves more likely. Amazon may reserve more when it believes future debits could outpace future credits, particularly when settlement timing is uncertain.

Unsettled disputes and delayed postings

Sometimes the provision is less about a new problem and more about unresolved old ones. If finance items are still pending, Amazon may hold funds until enough transactions clear to reduce its risk, or until disputes and offsets resolve.

Seller insight: when a provision appears, do not ask only “Is this valid?” First ask “What unresolved bucket is Amazon likely covering?” That question usually leads to the documents that matter.

Where to find it, and what to look for in the remittance trail

Most vendors first spot a provision inside remittance detail, often as a line item referencing provision for receivables. The exact presentation can vary, but the principle is the same. Amazon reduces available payment and records the reserve in the payment flow.

A practical review process:

Open Vendor Central and go to the relevant payment, remittance, or remittance detail view for the impacted period.

Pull the affected remittance and inspect all lines, not just the largest one.

Look for provision-related entries and any later reversal or offsetting entries.

Cross-check dates against returns, shortage activity, co-op postings, and promotional activity.

Compare the timing against prior remittances to see whether this is a new hold, a rolling reserve, or a partial release.

This is where audit amazon vendor central payments for overcharges becomes a real operating discipline. A proper audit is not just hunting for one bad line item. It is matching remittance movements to operational events and contractual terms.

A common mistake is reviewing one payment in isolation. Provisions often make more sense when viewed across several remittance cycles. One cycle shows the reserve. A later cycle may show the reversal, application, or partial release.

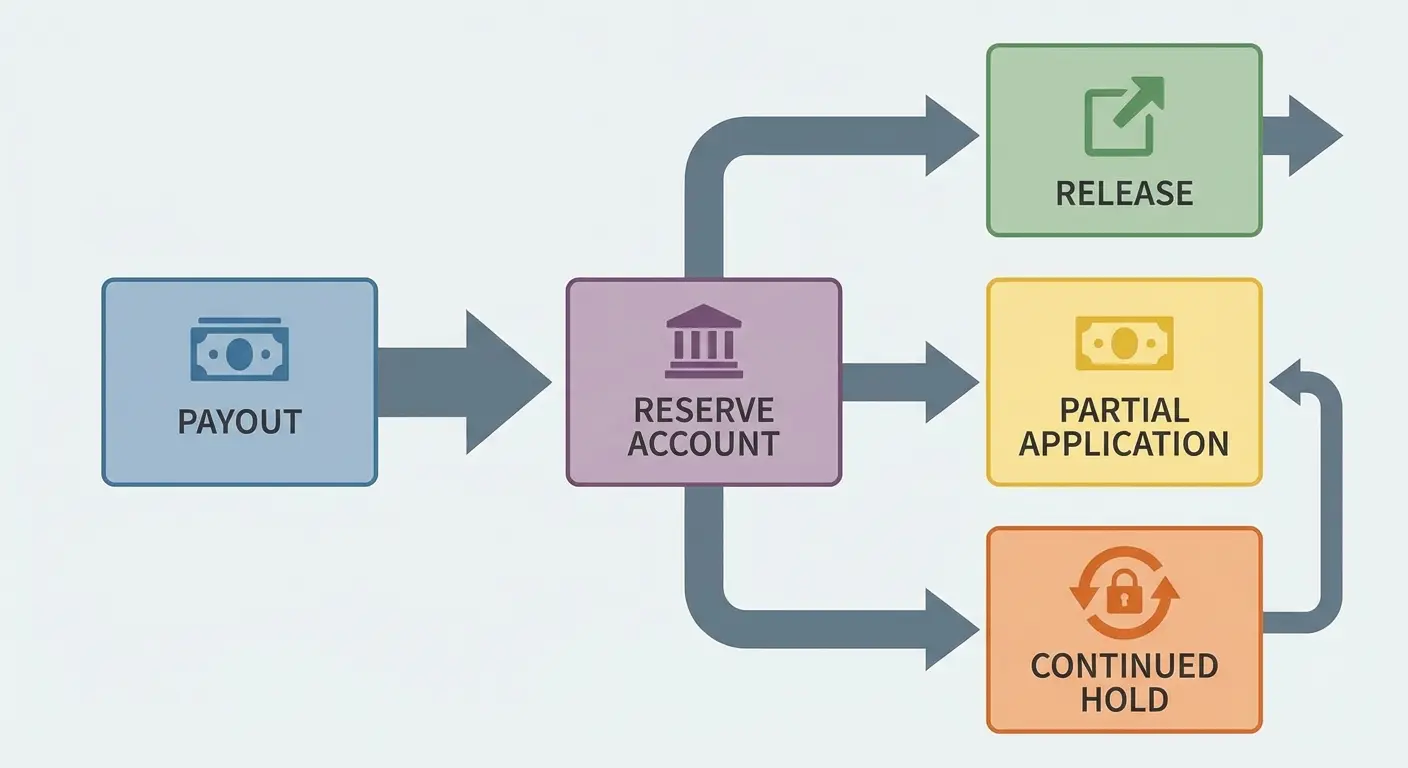

How the money moves in real life

The actual flow often looks like this.

Amazon identifies expected exposure on your account. It withholds part of your payout as a provision. That reserve sits while underlying items mature, such as returns, shortage-related items, co-op settlements, or other receivables. Then one of three things usually happens:

the reserve is released because the risk passed or the estimate was too high,

the reserve is partially applied to real deductions and partially released,

or the reserve remains because the underlying exposure is still unresolved.

This is why how long does amazon hold provision for receivables rarely has one clean answer. The duration depends on what the reserve is covering, how quickly the underlying transactions settle, and whether your account has continuing exposure.

In practice, holds may clear relatively quickly when tied to short-cycle settlement items. They can also persist across multiple payment periods when linked to returns windows, unresolved shortage activity, or pending finance cases.

When to reconcile, when to dispute, and when to escalate

Many vendors jump straight into disputing amazon vendor central provision for receivables as soon as they see the line item. Sometimes that is appropriate, but it is not always the most efficient first move.

A better sequence is:

Start with reconciliation

Before filing anything, identify the likely source of the reserve. Review:

recent shortage-related activity and case outcomes

return trends and any unusual return windows

co-op and allowance postings

promotional deductions or accrual timing

freight or compliance chargebacks, if present

unresolved invoice, deduction, or payment exceptions

If the provision appears consistent with known exposure, the immediate issue may be cash-flow planning and tracking, not a formal dispute.

Dispute when the reserve is unsupported, duplicated, stale, or excessive

You should move toward amazon vendor payment disputes best practices when you can show one of the following:

the provision appears tied to an issue already resolved

the same underlying liability seems reserved more than once

the amount is materially disconnected from observable exposure in the period you can document

the reserve has remained in place long after related items settled, with no credible remaining basis you can identify

related deductions were already paid or offset through another mechanism

Escalate when documentation exists but the case stalls

Finance cases often fail because the vendor is directionally correct but light on evidence. Escalation works better when you can present a clean packet: remittance IDs, invoice references, proof of delivery where applicable, shortage case outcomes, trade term support, and a timeline showing why the reserve should be released or reduced.

A useful heuristic: if you cannot explain the reserve in one sentence tied to one evidence set, your case is probably not ready.

Three short examples that mirror what happens on real accounts

A shortage-heavy account that mistakes reserves for fresh deductions

Hypothetical example: a vendor sees lower payouts over several cycles and assumes Amazon added new penalties. After review, the issue is a provision tied to a cluster of open shortage items. The right move is not arguing that the reserve “does not exist,” but proving that several shortage items were already invalidated and that the reserve should be recalculated.

This is a classic amazon 1p shortage claims and provisions guide scenario. The operational fix is to tighten proof-of-delivery retrieval where relevant and track shortage outcomes by remittance period.

A co-op-heavy business that cannot separate accrual from reserve

Hypothetical example: a vendor running frequent promotions sees both co-op deductions and a provision in the same window. They assume Amazon charged them twice for the same event. Sometimes duplication can occur, but often one line is an accrual or deduction tied to terms and the other is a temporary reserve against future receivables or offsets.

This is where understanding vendor central co-op and provision fees prevents false disputes. Map agreement terms, promo dates, accrual postings, and reserve timing before claiming duplication.

A valid dispute that wins only after a proper payment audit

Hypothetical example: a vendor performs a full remittance review and finds a provision that remained in place even though the related issues had already cleared. They assemble remittance history, prior case IDs, shipment records, and invoice references. After escalation, the reserve is released.

That is a practical model for how to reclaim money from amazon receivables provision. Reclamation usually comes from documented reconciliation, not from simply objecting to the label.

The misunderstandings that cost vendors the most

The first misunderstanding is treating every provision as a wrongful deduction. It may be wrong, but you have to test that conclusion against account activity first.

The second is ignoring provisions because they are “temporary.” Temporary holds still affect inventory purchasing, advertising budgets, and working capital.

The third is separating finance from operations. Provision activity often reflects receiving issues, shortages, returns behavior, or trade term complexity. If finance and operations are not sharing one ledger of events, patterns get missed.

The fourth is assuming Amazon will always clean it up automatically. Sometimes reserves unwind through normal settlement. Sometimes they persist until a vendor reconciles and follows up.

The fifth is doing shallow reviews. True amazon vendor central payment deductions explained work requires comparing remittances across time, not glancing at one statement and opening a generic case.

Where this gets messy: edge cases and practical limits

The hardest cases are not obviously wrong or obviously right.

One edge case is mixed-cause reserves. Amazon may hold one provision amount that reflects several categories of exposure at once. In those situations, there may be no single document that resolves the entire amount. You may need to break the reserve into probable components and support each with its own trail.

Another limit is visibility into Amazon’s estimation logic. Vendors often want a transparent formula. In practice, you may need to infer the rationale from surrounding remittance activity, deductions, and claim status.

There is also a timing problem. A reserve can be reasonable when placed and excessive later. That means the right challenge is often “this should have been updated after these issues cleared,” not “this should never have happened.”

For vendors with large catalogs, the account-level view can hide SKU-level drivers. A small set of ASINs with unusual returns, shortages, or allowances can affect payment behavior that looks portfolio-wide.

What a disciplined review process looks like

If you want a repeatable amazon vendor central financial reconciliation process, build it around monthly and remittance-cycle reviews rather than ad hoc fire drills.

A workable process usually includes:

a remittance tracker that flags all provision-related lines

a crosswalk to shortage items, returns, co-op, and promo activity

a log of reversals, releases, and aged reserves

standard evidence folders for proof of delivery, invoices, and case outcomes

thresholds for when finance monitors versus when leadership escalates

This is also the best way to audit amazon vendor central payments for overcharges without wasting time on noise. You are looking for aged reserves, duplicate exposure, stale holds, and reserves disconnected from known operational facts.

What to remember before the next payout lands

Use these points as an operational checklist:

what is amazon provision for receivables: a temporary reserve that can reduce a current payment while Amazon awaits settlement or coverage of expected receivables, offsets, or liabilities.

why is amazon withholding my payment for receivables: commonly because Amazon expects future charges, open claims, or unresolved exposure on the account.

amazon vendor central payment deductions explained: provisions, chargebacks, and co-op deductions can look similar on a remittance, but they behave differently and require different next steps.

difference between chargebacks and provision for receivables: chargebacks are typically assessed to a stated issue; provisions are typically broader reserves that may later reverse or apply.

how long does amazon hold provision for receivables: it depends on the settlement timeline for the underlying exposure and can span multiple payment cycles.

how to reclaim money from amazon receivables provision: reconcile remittance history to the underlying drivers, then pursue a documented release request when the reserve is unsupported, stale, duplicated, or excessive.

amazon vendor payment disputes best practices: lead with remittance IDs, invoice and shipment references, case outcomes, and a dated narrative that connects the reserve to the resolution.

amazon vendor central financial reconciliation process: connect payments to shortages, returns, co-op, and promotional activity so reserves do not linger unnoticed.

amazon 1p shortage claims and provisions guide: treat shortages and reserves as linked workflows, then track outcomes by remittance period.

understanding vendor central co-op and provision fees: separate contractual accruals from timing-based reserves before alleging duplicate billing.

disputing amazon vendor central provision for receivables: dispute after reconciliation, not instead of it, and focus on evidence that the reserve should be reduced or released.