Amazon Sales Tax Guide Canada for FBA Sellers

Olivia Reyes

Amazon sales tax guide Canada: What Experienced Sellers Actually Need to Get Right

If the CRA reviewed your last 12 months of Amazon payouts, would your GST/HST filings match line for line?

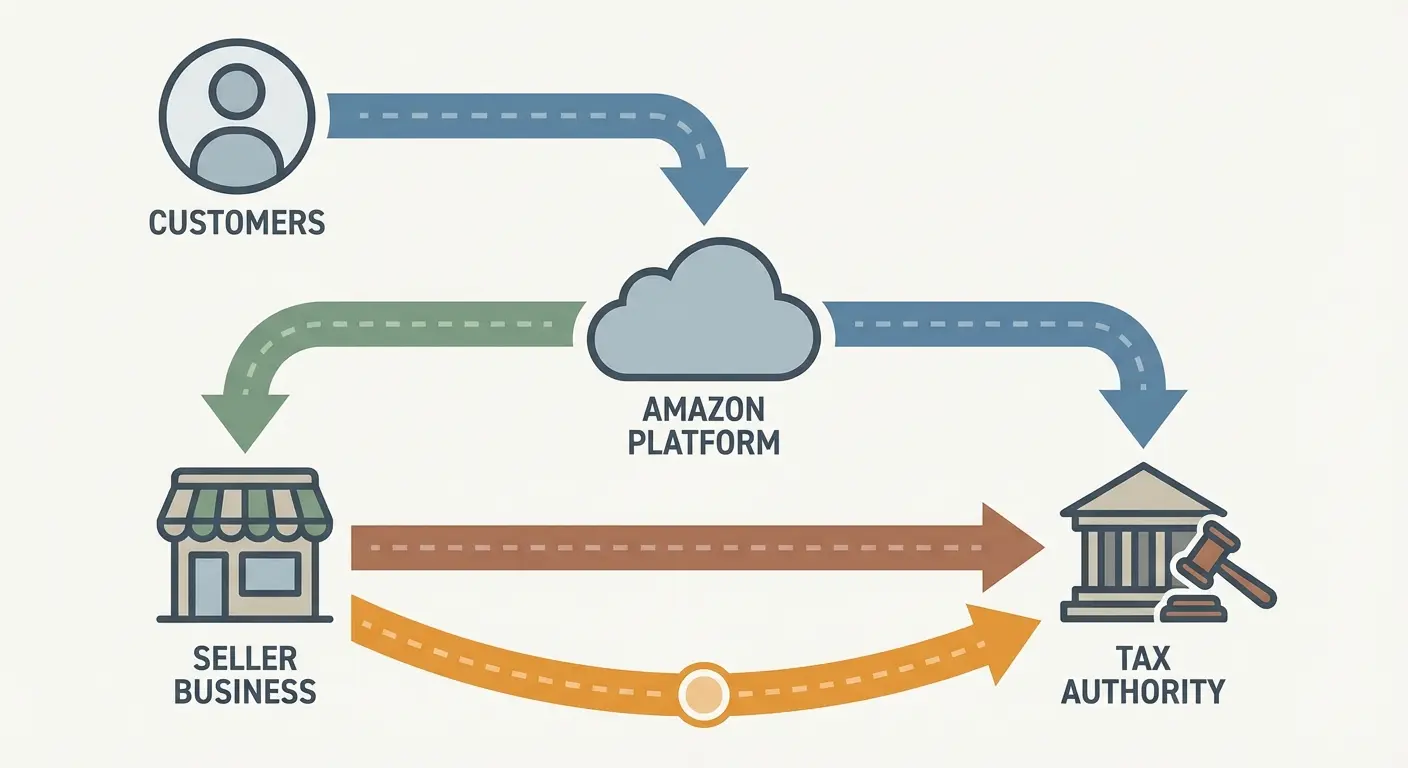

Many sellers assume Amazon is “handling the tax.” In practice, Amazon can calculate taxes at checkout, may collect and remit certain provincial taxes as a marketplace facilitator, and still leaves key filing and remittance obligations with the seller. This Amazon sales tax guide Canada is built for sellers who already understand FBA, margins, and cash flow, but want clarity on what actually matters for Amazon Canada tax compliance.

Below is a breakdown of how Canadian Amazon seller taxes typically work, how Amazon Tax Calculation Services fits in, what changes when you sell across borders, and where sellers get into trouble with audits and Input Tax Credits.

The Moving Parts Behind Canadian Amazon seller taxes

Before you optimize anything, map the full structure.

GST and HST: Federal and harmonized sales tax

GST (5%) applies across Canada. HST combines GST with a provincial portion and applies in participating provinces, commonly at 13% or 15%.

For many registered sellers:

Amazon calculates GST/HST based on the buyer’s delivery address and the tax settings you provide.

The tax is collected from the customer at checkout.

You remain responsible for filing and remitting your GST/HST, unless a specific rule shifts remittance to the platform for a specific tax type.

A key point for compliance: do not assume that because Amazon calculated and collected an amount, it has also been remitted on your behalf. Confirm remittance responsibility by tax type and province, then align your filings to that reality.

PST and QST: Provincial layers

This is where Amazon Canada marketplace facilitator rules can matter most.

PST (such as BC and SK): in some provinces, marketplace facilitator rules require the marketplace to collect and remit PST on marketplace sales made through the platform. The exact scope depends on the province and the nature of the sale.

Manitoba’s RST: similar marketplace rules can apply.

QST (Quebec): Quebec has its own rules and registration requirements. For some marketplace sales, the platform may be required to collect and remit QST, but seller circumstances can vary, especially for sellers registered for QST and for certain transaction types.

Because these rules can change and vary by province, build your process around Amazon Canada PST QST rules as they apply to your listings, your registration status, and where your customers are located. Do not rely on a blanket assumption that “Amazon handles provincial tax everywhere.”

The CAD $30,000 threshold and registration

For GST/HST, if your worldwide taxable supplies exceed CAD $30,000 in a single calendar quarter or over four consecutive calendar quarters, registration is generally required. Below that threshold, registration is generally optional.

Voluntary Amazon GST HST registration can still be financially sensible earlier than many sellers expect, especially if you pay meaningful GST/HST on ads, fulfillment fees, software, professional services, and import GST. Without registration, you generally cannot claim Amazon seller Input Tax Credits for those expenses.

How Amazon calculates and reports tax

Understanding Amazon seller tax calculation setup is not optional. It affects both compliance and margin accuracy.

Step 1: Tax settings and product taxability

Amazon Tax Calculation Services helps determine:

which tax applies (GST, HST, and potentially provincial sales taxes depending on province and rules),

the rate based on destination,

whether tax is charged at checkout based on the settings and product taxability classifications provided.

If the configuration is off, you can under-collect tax and owe it out of pocket, or over-collect and create reconciliation and customer experience issues.

Product classifications matter. If your catalog includes items that may be zero-rated, exempt, or taxable at different rates, using a single generic classification can create errors. If you are uncertain about an item’s tax status, confirm it before assigning product tax settings.

Step 2: Collection vs. remittance

Collection and remittance are separate concepts.

Collection: Amazon charges the customer at checkout.

Remittance: either the marketplace remits (where marketplace facilitator rules apply) or you remit through your tax return.

Amazon reports tax-related amounts in settlement and tax reports. Reporting is not filing. Your process should include:

reconciling Amazon tax reports to accounting records,

filing the correct returns based on your registrations,

remitting on your assigned frequency (monthly, quarterly, or annually), and on time.

Step 3: Sales tax on Amazon fees

Amazon commonly charges GST/HST on many seller-facing fees, which may include:

referral fees

FBA fulfillment fees

storage fees

advertising

certain subscription services

If you are registered and the expenses are for your commercial activities, those amounts can often be recoverable as Amazon seller Input Tax Credits. If you are not registered, they are generally just an added cost.

Input Tax Credits: Where experienced sellers win or lose

Input Tax Credits are the mechanism that can prevent tax cascading. When you pay GST/HST on eligible business inputs, you can generally claim that amount as an ITC to offset GST/HST you must remit.

Example structure:

You collect $10,000 in GST/HST from customers.

You paid $3,000 in GST/HST on eligible expenses such as Amazon fees, advertising, freight, software, and import GST.

You remit $7,000 net, assuming the ITCs are properly supported and claimed.

If you miss those ITCs, you can over-remit.

Import GST and FBA inventory

For Canada import taxes FBA, tracking is especially important.

If you import inventory into Canada and you are the importer of record:

you may pay GST at the border,

that import GST is often claimable as an ITC if you are registered and you retain proper import documentation,

customs duties are not GST/HST and are not claimed as ITCs.

A common bookkeeping problem is rolling import GST into inventory cost without capturing it as a recoverable tax component. Track import GST separately and retain supporting documents.

cross-border Amazon seller taxes: When it gets complex

Selling across Amazon.ca and Amazon.com, using remote fulfillment programs, or holding inventory in multiple countries can make cross-border Amazon seller taxes layered quickly.

Common issues include:

importer of record status and documentation

GST/HST registration requirements for non-residents that store inventory in Canada or otherwise carry on business in Canada

U.S. state sales tax obligations when selling into or within the U.S.

entity structure and intercompany flows if you operate multiple entities

A U.S. seller with inventory stored in Canada can have Canadian registration obligations depending on their facts, including where inventory is held, who is making the supply, and whether the seller is considered to be carrying on business in Canada.

On exports, some sales may qualify for zero-rating, but documentation is critical. Keep evidence that goods were shipped from Canada to a destination outside Canada, and ensure invoicing and records support the tax treatment.

What a CRA Amazon seller audit typically looks for

A CRA Amazon seller audit often starts with data matching and reconciliation.

The CRA may request:

Amazon sales reports

settlement reports

tax reports

bank statements and deposits

import and customs documentation

invoices supporting ITCs

They commonly test consistency between:

gross sales on Amazon reports

reported taxable sales

reported GST/HST collected or payable

claimed ITCs and supporting invoices

Common risk areas include reporting sales lower than marketplace gross sales without clear adjustments, or claiming ITCs that are high relative to the business profile without strong documentation.

Organized records help. Separate tracking for marketplace-facilitator remitted taxes, GST/HST you must remit, zero-rated exports, and ITCs by category improves defensibility in a CRA Amazon seller audit.

Practical scenarios sellers face

Case 1: The growing private label brand

A Canadian FBA seller crosses the small supplier threshold and delays registration.

Once registration is required, the seller can have liability for GST/HST on taxable supplies from the effective date they were required to be registered, not simply from the date they finally registered. The practical impact is that if tax was not charged and collected during that window, the seller may have to fund it.

Case 2: The high ad-spend seller

A brand spends heavily on Amazon PPC and other advertising that includes GST/HST.

They are registered but do not reconcile fee tax and advertising tax, so they under-claim ITCs for multiple filing periods. The result can be over-remittance and reduced working capital.

Case 3: Inventory imported into Canada for FBA

A seller imports inventory, pays import GST, and records the entire landed cost as inventory.

At filing time, they fail to claim the import GST as an ITC. This can cause a cash-flow hit because import GST was paid, and then GST/HST collected is remitted without the intended offset. Separate and support import GST properly.

Where sellers get tripped up

“Amazon remits all my sales tax”

That is often incorrect. Under marketplace facilitator rules, Amazon may remit certain provincial sales taxes on marketplace transactions in specific provinces and circumstances, but sellers commonly remain responsible for filing and remitting GST/HST, and sometimes QST, depending on the transaction and rules in effect.

Treat this as a verification task, not an assumption. The right answer depends on the tax type, the province, and your registration status.

“If Amazon calculates it, I’m covered”

Amazon seller tax calculation setup reduces errors but does not remove responsibility. If your settings or product taxability classifications are wrong, the liability can still fall on you.

“If I’m under $30,000, I should avoid registration”

Optional registration can be a smart financial move for sellers with meaningful GST/HST-bearing expenses, including import GST and advertising. If you are not registered, you generally cannot recover those amounts through ITCs.

“Audit risk is low for small sellers”

Audit selection is risk-based. Marketplace records are highly structured and reconcilable, so basic mismatches can be easy to detect. Solid recordkeeping matters early.

The edges that need extra attention

Multiple warehouses across provinces

Where inventory is stored can affect nexus-style considerations for provincial registrations and may influence how you assess your obligations, even when destination-based rules drive tax charged to customers. Review warehouse footprint alongside sales patterns.

Bundles and mixed taxability

Bundles that mix zero-rated and taxable items can require careful tax analysis. A single default classification can misapply tax. Ensure the structure of the bundle and pricing supports the intended treatment.

Non-resident sellers

Non-resident sellers using Canadian fulfillment can still have Canadian obligations. The key question is often whether the seller is carrying on business in Canada and making taxable supplies there, which can depend on inventory location and fulfillment structure.

Building a clean, defensible setup

For Amazon Canada tax compliance, aim for repeatable structure.

At minimum:

register on time for GST/HST, and for QST if required based on your facts

confirm how marketplace facilitator rules apply to your sales by province

configure Amazon Tax Calculation Services correctly

maintain accurate product taxability settings for the catalog you sell

reconcile Amazon reports monthly to accounting records

track ITCs separately by category, including fees, ads, and import GST

ensure returns filed align to the data you can substantiate

This is also where Amazon Tax Calculation Services helps most when it is paired with disciplined reconciliation rather than treated as autopilot.

What matters most

If you remember nothing else from this Amazon sales tax guide Canada, focus on these:

GST/HST collected through Amazon is commonly the seller’s responsibility to report and remit, even when Amazon calculates it.

Marketplace facilitator treatment varies by province and tax type, so Canadian Amazon seller taxes require province-by-province verification.

Accurate Amazon seller tax calculation setup, including product classifications, directly affects both compliance and customer-facing tax charged.

Amazon seller Input Tax Credits on fees, ads, and import GST can materially affect cash flow when supported and claimed correctly.

Canada import taxes FBA require clean documentation; duties are not ITCs, and import GST is often claimable when you are the importer of record and registered.

cross-border Amazon seller taxes escalate quickly and should be reviewed before expanding inventory and fulfillment footprints.

Monthly reconciliation is one of the strongest defenses if a CRA Amazon seller audit begins.

Build your process so it is defensible even when volumes scale. That is the difference between reactive cleanups and controlled compliance.